Intro

In Part 1, we explored the rationale behind selecting MegaETH as the first subject for pre-TGE token valuation and examined its fundamentals, including the Tech Stack, Team, Competitor Analysis, and Ecosystem.

Part 2 will delve into the tokenomics analysis and present the valuation of the $MEGA token from six different perspectives.

Thanks for reading jellulu_fish's Substack! Subscribe for free to receive new posts and support my work.

Key Takeaway

MegaETH has succeeded in reducing block time to 0.01 seconds to create a real-time blockchain.

Judging by the results of the public sale and pre-deposit, MegaETH appears capable of entering the ranks of the top 14 chains upon mainnet launch.

Due to MegaETH’s tokenomics structure, short-term dumping is expected to be minimal. Long-term utility and revenue are strong, but the token deflation aspect is judged to be weak.

The most agreed-upon valuation for $MEGA is $2B ~ $2.3B. However, if market recovery and revenue-based value capture proceed smoothly, the author views $4B as the base valuation.

Furthermore, if MegaETH proves PMF (Product-Market Fit) as a differentiated L2 and achieves growth beyond expectations, there is room for upside from $6B to $12B.

(※ Due to the length of this article, I intend to publish it in two parts. Part 1 covers the fundamental background of MegaETH (Tech Stack, Team, Competitor Analysis, and Ecosystem), while Part 2 will address the tokenomics analysis and the $MEGA token valuation analyzed from six different perspectives.)

Tokenomics Analysis

1) MegaETH Tokenomics Overview

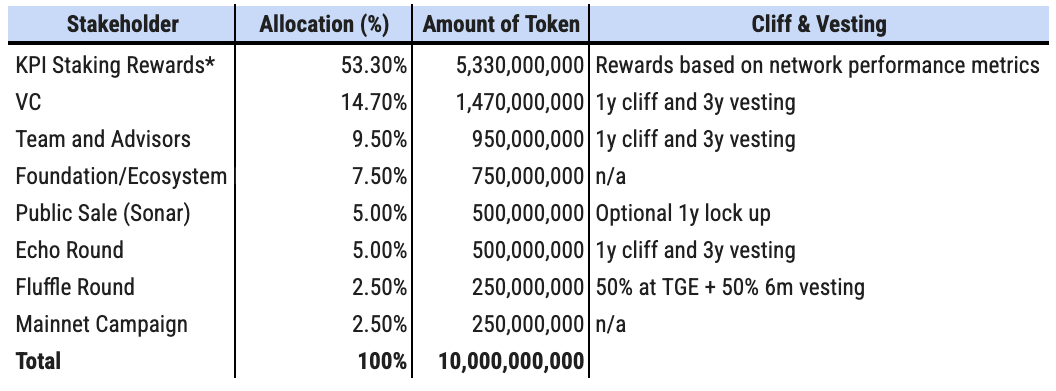

a) Max Supply Amount: 10B

b) Allocation & Distribution: 75.8% for community

MegaETH features a unique token distribution model known as KPI Staking Rewards, which accounts for 53.3% of the total token supply. These rewards are distributed exclusively to $MEGA stakers and are allocated based on network metrics rather than a simple time-based schedule. The Initial Measurement Metrics/Areas are as follows:

Ecosystem Growth

Technical Performance

MegaETH Decentralization

Ethereum Decentralization

c) Utility

① Gas Fee Payment: Selectable between ETH and MEGA.

③ Protocol Governance Participation.

② (Future Roadmap) Sequencer Participation Staking: Once the rotation mechanism is implemented after the mainnet launch, $MEGA tokens will be used for staking to participate as a rotating sequencer.

⑤ (Future Roadmap) Ultra-low Latency Sequencer Adjacency Staking: Latency-sensitive builders will competitively stake $MEGA to secure a position physically/network-wise closest to the active sequencer to guarantee faster processing.

d) Main revenue model

Sequencer Margin:

The basic/main revenue model for most L2s.

The difference between L2 transaction gas fees collected by the Sequencer and the settlement costs of posting data to Ethereum L1.

Profit = User Transaction Fees (L2) - Ethereum L1 Data Costs

USDm Interest Revenue:

Interest revenue (yield) generated from USDm’s collateral assets (US Treasuries, etc. RWAs).

Part of this revenue will be used to cover Sequencer operating costs, thereby providing users with gas fees at cost or near-zero levels.

e) Value capture model

Fee Burning: Possibility of introducing a Fee Burning mechanism to offset inflation from staking rewards (requires governance approval).

f) Others

Compliance: MegaETH released a MiCA-compliant tokenomics whitepaper before the public sale. MiCA is a bill for protecting virtual asset investors, requiring transparency of information and strict legal liability for issuers. The most notable difference between MiCA-compliant and non-compliant projects is the ‘14-day refund guarantee’.

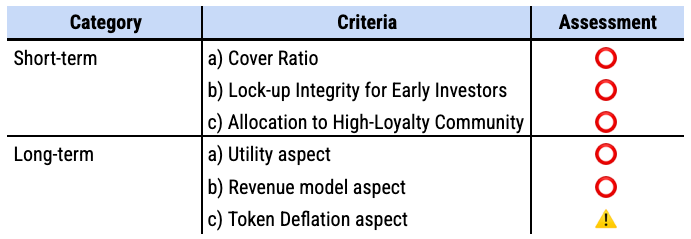

2) Short/Long-term Tokenomics Health Assessment

Primarily, projects issuing tokens (or investors in those tokens) worry about one thing: When will the price crash? Short-term crashes occur when many existing token holders have incentives to dump immediately after TGE. Long-term crashes happen if the project loses competitiveness in the future market or if the value created by the project is not well-captured by the token. If even one of these applies, valuation based on the project’s fundamentals becomes meaningless.

Overview and Criteria

Short-term: Evaluation of dumping by pre-TGE token holders

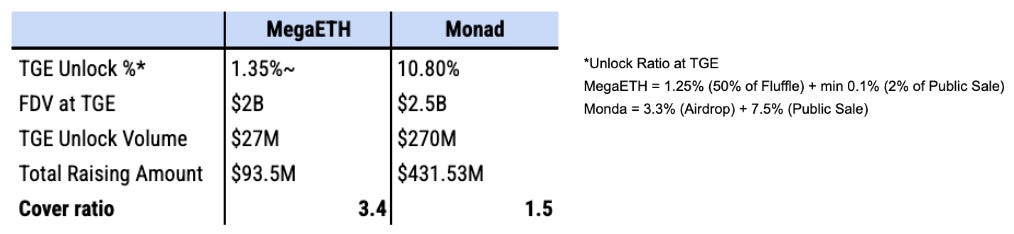

a) Cover Ratio: ⭕

Definition

Cover ratio = Team Raise Amount (Defense Fund) / Initial Sell Pressure

A ratio < 1 indicates a risk of price crashing due to high sell pressure at TGE

Current Estimate: ~3.7 (Safe)

With a ~$90M raise and a $0.2 futures price, the team can absorb the sell pressure

Initial Unlock is estimated at ~1.35% (135M MEGA).

Fluffle Round: 1.25% (2.5% * 50%)

Public Sale: est. min 0.1%

(Note: The exact unlock % is undisclosed. However, assuming 73% of participants received the minimum allocation (2,650 MEGA) and unlock fully, this amounts to at least 10M MEGA)

There is no airdrop allocation

Risk Factors (Ratio < 1):

If the token price exceeds $0.7 at TGE

If the immediate Public Sale unlock exceeds 75%

Comparison with another project:

Monad, which recently conducted its TGE, also maintained a Cover ratio greater than 1, but MegaETH is situated in a significantly more secure range

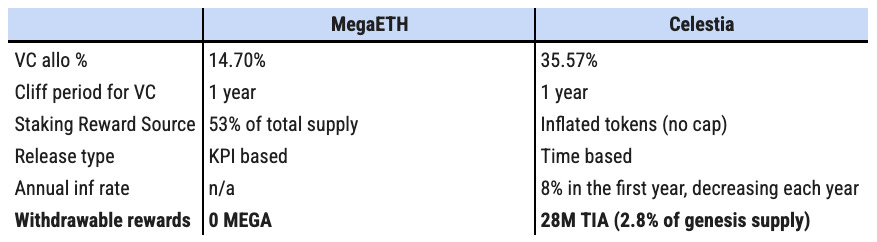

b) Lock-up Integrity for Early Investors: ⭕

Strict Schedules: Seed/Echo investors face a 1-year cliff, while Fluffle investors have a 50% TGE unlock with 6-month vesting. Notably, ~20% of public sale participants also opted for a 1-year lock-up.

Closing the “Celestia Loophole”: In Celestia’s case, VCs recouped their principal during the lock-up period by withdrawing liquid staking rewards (approx. $64M value vs $56M raise).

MegaETH’s Solution: MegaETH enforces the underlying lock-up terms on staking rewards. Rewards generated from locked tokens cannot be withdrawn immediately, preventing sell pressure from accrued interest.

c) Allocation to High-Loyalty Community: ⭕

Transparent & Bimodal Distribution: MegaETH emphasized fairness during the public sale using a bimodal structure that balances broad ownership with loyalty-based weighting.

Targeted Allocation Criteria:

25% (Long-term Supporters): Prioritized based on past engagement in MegaETH/Ethereum communities, social media activity, and GitHub contributions.

75% (Activity Based): Distributed via a comprehensive evaluation of on-chain activity, testnet participation, and off-chain engagement (e.g., Twitter, Kaito scores).

Incentivizing Commitment: Participants opting for a 1-year lock-up received a 10% discount/bonus and higher allocation probability, effectively targeting early contributors and long-term believers.

Long-term: Evaluation of value capture flywheel potential

a) Utility aspect: ⭕

Unlike existing L2s, MegaETH plans to use the MEGA token for sequencer decentralization beyond simple governance.

Specifically, depositing tokens will be required to participate as a sequencer or to use a nearby sequencer in the future, so demand for the token is expected to increase as the network grows.

However, it seems it will take quite some time for this utility to be implemented (planned to use a single sequencer at initial launch).

b) Revenue model aspect: ⭕

Generally, stablecoin revenue is overwhelmingly larger than sequencer margin.

Comparing Base and Arbitrum, which generate the most tx and revenue in the rollup ecosystem, to Ethena, shows a 5x to 10x difference.

The stablecoin business has a much more advantageous structure than the L2 infrastructure business in terms of margin rate and scalability of the business model itself.

Accordingly, if stablecoin issuance within MegaETH occurs smoothly in large quantities, it is expected to far exceed existing L2 revenues.

c) Token Deflation aspect: ⚠️

MegaETH plans to reduce gas fees to near-zero levels as revenue from USDm increases.

Accordingly, as gas fees decrease, fee burning will also decrease, so the deflationary effect is seen as minimal.

Summary)

In summary, structurally, MegaETH is not expected to have severe short-term dumping, and a positive flywheel is expected in terms of utility and revenue in the long term. The downside is that since the project’s revenue flows more into the ecosystem rather than being directly returned to token holders, the value capture of the token itself could be weak. Therefore, simple fee burning is judged to be insufficient, and supplementary mechanisms for token price management seem necessary in the long term.

Valuation

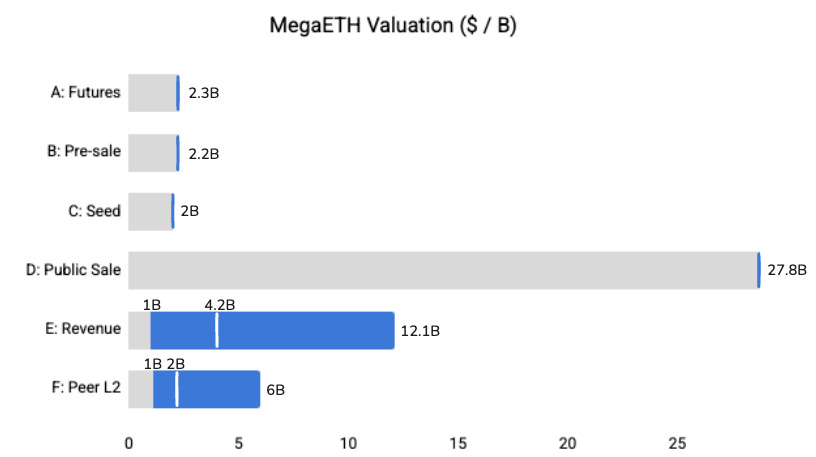

1) A: Futures Trading Price

The futures trading price of a pre-TGE token reflects market participants' expectations for the initial circulating market capitalization. If this price persists until listing, market makers are likely to form spreads around it. Consequently, these prices serve as a valuable indicator for predicting ultra-short-term price movements immediately following the TGE.

Currently, $MEGA is traded on five exchanges, with Hyperliquid commanding more than half of the volume. Although the price reached a high of $0.7, it held steady in the $0.22 - $0.235 range these days. This zone represents the "Base Consensus" where early buyers felt comfortable.

→ [A: $2.3B]

2) B: Pre-market Price

On Whales Market, pre-TGE tokens can be traded based on ICO allocation or pre-token (or point) collateral.

Although the price consolidated around the $0.33 level for an extended period, trading volume was minimal. Consequently, the $0.22 range—which recorded the highest recent buying volume—can be considered the level where the market’s base consensus has formed.

→ [B: $2.2B]

3) C: Private Sale Based Price

MegaETH raised a total of $30M across the Seed and Echo rounds, both at a $200M valuation. The Seed round serves as a critical milestone. It signifies that professional VCs—rather than just friends or angels—have validated through due diligence that the team’s vision is ‘worth betting on.’

However, at this stage, hypotheses remain unverified and Product-Market Fit (PMF) is still being explored. Due to these high risks, the valuation is set conservatively. Top-tier crypto VCs, such as Dragonfly, typically target at least a 10x return to compensate for this risk premium. Working backwards from this target, the Implied Fair Value expected by investors is approximately $2.0B ($200M x 10)

→ [C: $2B]

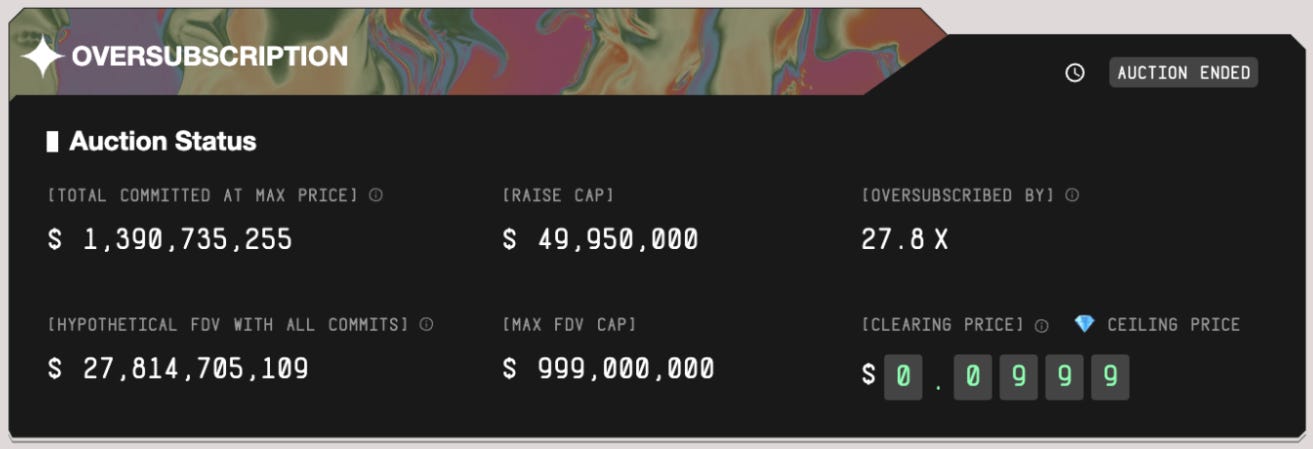

4) D: Public Sale Based Price

MegaETH’s public sale was heavily oversubscribed, exceeding the $50M target by 27.8 times. With approximately $1.39B committed for just 5% of the total supply, the implied FDV reaches a massive $27.8B.

(FDV Calculation: 1,390,735,255 / 0.05 = 27,814,705,109)

However, this figure should be interpreted with caution. It likely reflects inflated demand from participants using multiple accounts (Sybil attacks) to maximize their allocation chances, making it less reliable than other valuation models.

→ [D: $27.8B]

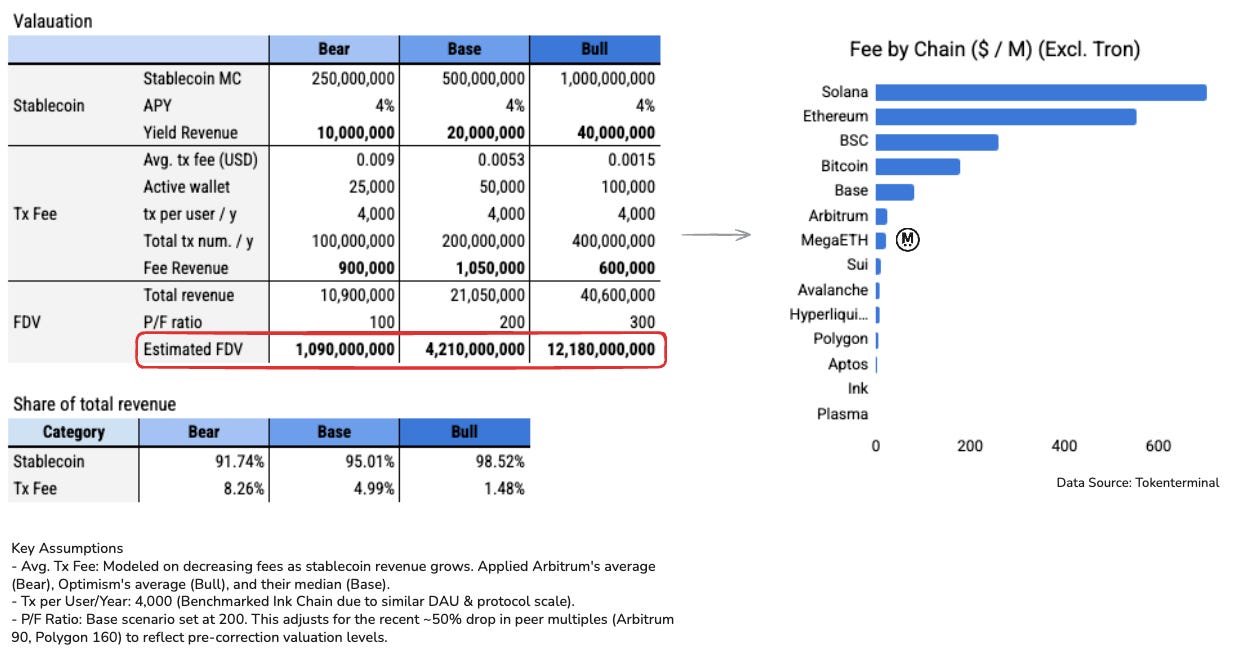

5) E: Potential Revenue Based Price (12 months later)

MegaETH’s revenue model is twofold, consisting of Sequencer Margin (transaction fees) and Stablecoin Yield (interest from USDm collateral). Based on the expected traction analysis, I drafted Bearish, Base, and Bull scenarios.

Notably, Across all scenarios, stablecoin yield accounts for over 90% of total revenue. Even, the total revenue projected in the Base scenario ($21.05M) positions MegaETH near the median revenue of the top 14 chains by TVL (comparable to Polygon’s $21M or Arbitrum’s $24.4M). This is significant because MegaETH achieves this revenue scale not by relying solely on sequencer margins—which are constrained by gas fee competition—but by adopting a highly scalable stablecoin-based revenue model.

Scenario Breakdown:

Bearish Case: Assumes stablecoin issuance meets only the initial pre-deposit cap of $250M.

Revenue: ~$10.9M (Yield: $10M / Fees: $0.9M)

Valuation: Applying a conservative P/F ratio of 100 (reflecting current depressed L2 multiples like Arbitrum’s ~90) results in an FDV of ~$1B.

Base Case: Assumes issuance reaches $500M, the amount actually filled just before the pre-deposit closed.

Revenue: ~$21.05M (Yield: $20M / Fees: $1.05M)

Valuation: With a P/F ratio of 200, the estimated FDV is ~$4.2B.

Bull Case: Assumes the full pre-deposit max cap of $1B is utilized.

Revenue: ~$40.6M (Yield: $40M / Fees: $0.6M)

Valuation: With a premium P/F ratio of 300, the FDV could reach ~$12.1B.

→ [E: $1B / $4.2B / $12.1B]

6) F: Relative Comparison with Similar L2s

Based on the outlined scenarios, I benchmarked MegaETH against comparable L2 chains. It is important to note that a project’s FDV is not strictly proportional to its metrics. Even with similar traction, value capture can diverge significantly due to differences in tokenomics and market sentiment.

Mantle serves as a prime example. Despite recording lower TVL and revenue than Polygon or Arbitrum, it commands the highest FDV among L2s. This valuation premium is driven by effective supply control (via high staking APY) and growth expectations from its Bybit integration.

Consequently, I established the following comparative baselines:

Bear & Base Cases: Compared with Polygon ($1.1B) and Arbitrum ($2B), which exhibit similar revenue profiles in these scenarios.

Bull Case: Compared with Mantle ($6B), reflecting a scenario where the project successfully captures a high valuation premium.

→ [F: $1.1B / $2B / $6B]

Summary)

In summary, the comprehensive valuation results for MegaETH are as follows.

Market Consensus Group: $2.0B ~ $2.3

The value where most indicators coincided: A (Futures: 2.3), B (Pre-sale: 2.2), C (Seed: 2), F-2 (Peer Value Base: 2)

This suggests that the strongest Fair Value for MEGA currently thought by the market and early investors is between $2.0B ~ $2.3B.

Target Fair Price and Upside Potential: $4B ~ $12B

The Base scenario is drawn based on figures MegaETH has already achieved, allowing for an expectation of a fair value of $4B based on Base scenario fundamentals.

Should the market recover, leading to expanded L2 P/S multiples, and the project effectively captures value by mitigating token inflation, the valuation has the potential to scale towards the Bull scenario of $6B to $12B+

Outlier: D ($27.8B)

The ‘total committed amount’ of the public sale is an indicator of “Market Demand Strength” rather than actual corporate value.

Needs to be excluded when calculating fair valuation.

Volatility Range: $1.0B ~ $12B

Since E-1 ($1B) and F-1 ($1.1B) appear similar, the downside is open up to $1.0B in the worst case.

On the other hand, the Bull Case has the potential to expand from $6B to $12B.

Risk

MegaETH is currently a highly spotlighted L2, but risks still exist internally and externally. These are as follows:

The mainnet is not yet live; performance scalability and stability remain unproven in a production environment.

Reliance on a single sequencer during the initial launch phase poses temporary centralization and censorship risks.

The abrupt termination of the pre-deposit campaign—involving cap adjustments and subsequent refunds—raises questions regarding operational maturity.

The L2 narrative has cooled amidst fierce competition. The current landscape suffers from an oversupply of infrastructure relative to applications, exacerbated by low switching costs for users.

The entry of giants like Stripe, Circle, and Kraken—who already possess established product-market fit (PMF) and deep liquidity—presents a significant barrier to MegaETH’s “0-to-1” ecosystem growth.

Market skepticism persists regarding the ability of infrastructure layers (chains) to capture value effectively compared to application-layer protocols.

Patient capital is scarce thesedays. According to Keyrock and Memento Research, most tokens launched last and this year are trading below their TGE price, with most experiencing sharp declines within 15 days of listing.

Conclusion

MegaETH is cited as the most anticipated TGE project of 2026. While everyone’s reason for being bullish on MegaETH may be different, the major strengths of MegaETH that I think of are as follows:

Not just faster than existing chains, but implementing Web2 real-time literally on-chain.

Building services that can exist ‘only’ on MegaETH through the MegaMafia program

Strong community and transparent communication from key members to maintain and improve community trust.

While the latter two are non-technical “soft power” advantages, they are crucial for maintaining user retention in a market where post-TGE attention typically fades rapidly.

My conviction was further reinforced during the pre-deposit phase. Despite securing $500M in mere seconds, the team chose to return all funds. While some criticized this as operational inexperience, the incident actually highlighted the project’s integrity. Shuyao Kong’s subsequent statement perfectly encapsulated their philosophy of sustainable growth:

“The 500M that came in, although it instantly propelled us to the top five in the public chain revenue rankings, we are very clear in our hearts that this kind of money that comes in under such circumstances is, for the Mega team, a debt.

In the end, a healthy ecosystem should grow bit by bit and try to avoid peaking right at debut.” - Shuyao Kong

As Vitalik stated in Endgame, we must be “open to all of the futures, and does not have to commit to an opinion about which one will necessarily win.” In this spirit, rather than dismissing new chains due to challenging market conditions, we should evaluate the potential of ecosystems like MegaETH with an open mind.

I look forward to MegaETH’s successful mainnet launch and its journey toward sustainable growth.

Disclaimer

The author personally participated in MegaETH’s public sale and is a pre-TGE token holder.

This valuation is for the purpose of ‘estimating’ what value might be appropriate through relative comparison with other projects, as there are not enough statistical figures (e.g., 3-year revenue, cost data) before MegaETH lists.

Please be aware that the assumptions used in the valuation and the Buy/Sell ranges under that valuation are all written under the author’s subjective judgment, and clearly state that the actual value of the MegaETH token may not flow as below.

Therefore, I inform you that this is not a recommendation to buy or sell a specific asset. NFA, DYOA. Also, since it is assumed that market conditions after MegaETH’s token launch will occur amidst a crypto bear market like now, I notify that such valuation may be largely meaningless if a crypto bull market unfolds due to macro issues, etc.

Thanks for reading jellulu_fish's Substack! Subscribe for free to receive new posts and support my work.